Middle East linked disruption extends well beyond the region, with growing implications for global supply chains.

As capacity tightens, routes are reconfigured and costs come under pressure, supply chains are entering a more complex and less predictable phase.

Air freight capacity tightens

Air freight markets are among the most immediately affected. Reduced capacity through key Gulf hubs — which typically handle a significant share of global cargo flows and particularly Asia — has forced airlines to reroute services and limit network coverage.

Market data indicates that capacity reductions in parts of the Middle East and South Asia have been significantly steeper than the decline in volumes, creating a sharp imbalance between supply and demand. As a result, rates on some key east–west corridors have risen by more than 50% week on week, with spot pricing increasing at an even faster pace.

Cargo is increasingly being redirected via alternative gateways such as China and Hong Kong, placing additional pressure on corridors that were previously less affected. This is tightening capacity across Asia–Europe routes and contributing to delays, space shortages and short-notice schedule changes.

At the same time, rising fuel costs and the introduction of war risk-related surcharges are adding further upward pressure, while rate validity is shortening as carriers respond to rapidly changing conditions.

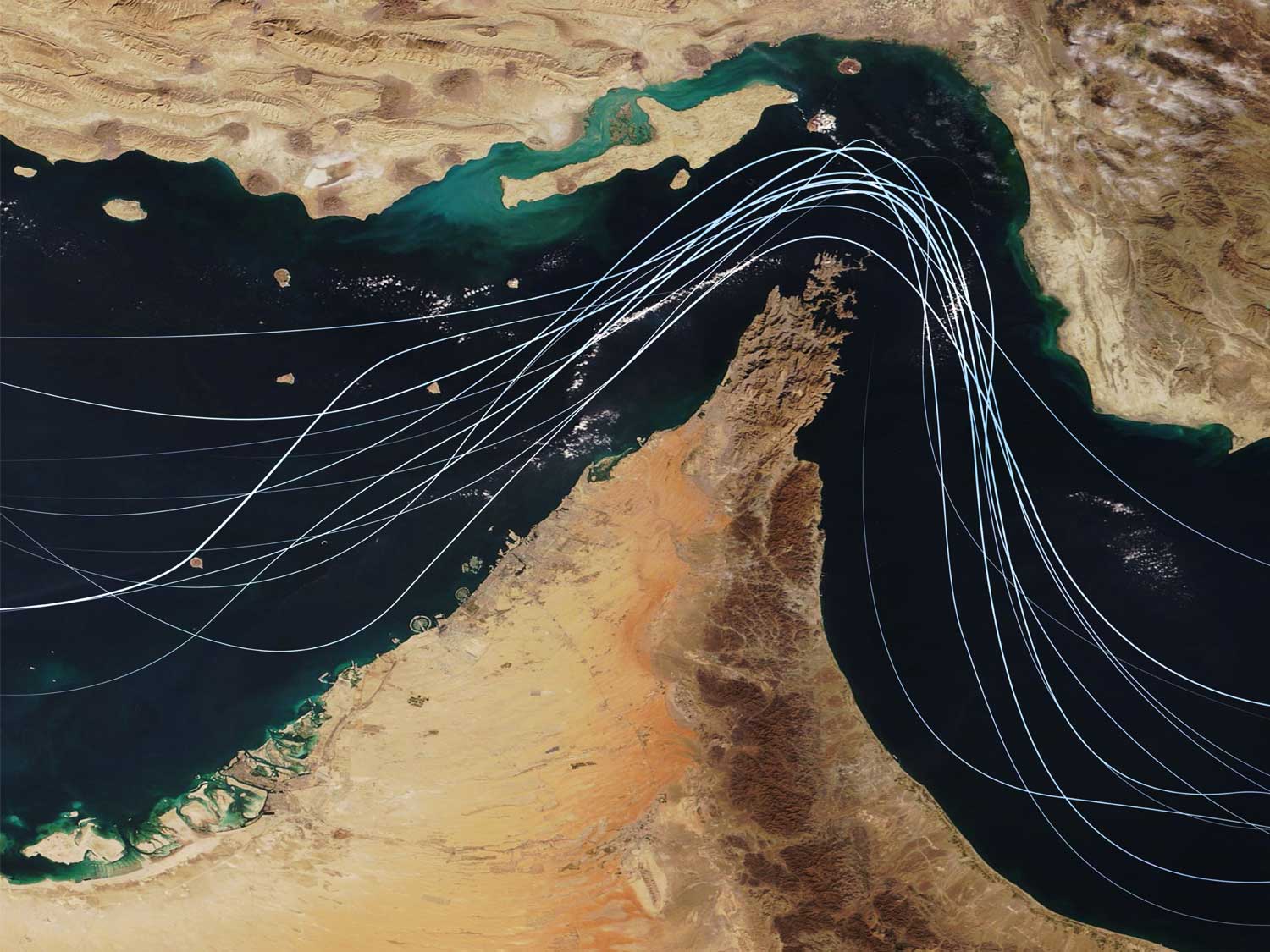

Ocean disruption drives congestion, diversion and equipment imbalances

Ocean freight is facing a different but equally significant set of challenges. The effective closure of the Strait of Hormuz — a corridor that typically handles a substantial share of global energy flows — has led to a dramatic reduction in vessel transits, with movements down by around 95% compared to normal levels.

Shipping lines have suspended services into the Arabian Gulf and are diverting vessels to alternative ports, where cargo is being discharged and held for onward movement. This is creating a knock-on effect across surrounding regions.

Ports outside the Gulf are now absorbing unexpected volumes. Congestion levels at key contingency hubs have reached critical levels, with some locations operating at or near full capacity and vessel waiting times extending well beyond normal ranges.

At the same time, an estimated 200,000+ TEU of capacity remains effectively trapped within the Gulf, contributing to equipment shortages in Asia as empty containers are unable to return to origin markets. This imbalance is expected to place further pressure on export flows in the coming weeks.

Rising bunker costs are also beginning to influence vessel operations, with some operators reducing sailing speeds to manage fuel consumption, adding further variability to transit times.

Costs rise as surcharges and fuel pressures build

Across both air and ocean freight, cost pressure is becoming more pronounced. Emergency surcharges linked to fuel volatility, war risk and network disruption are being introduced or expanded across multiple trade lanes.

Air freight rates have already increased sharply on key routes, while ocean carriers are implementing additional charges to reflect higher operating costs and longer routing distances. In parallel, regulatory scrutiny is increasing, particularly around how surcharges are applied and communicated.

For shippers, this is creating a more complex cost environment, where pricing can change quickly and visibility is reduced.

The past few weeks have highlighted how quickly supply chain assumptions can change and how important it is to have flexible, well-informed contingency options in place.

Metro is supporting customers by identifying alternative routings, securing capacity across air and ocean networks, and maintaining close operational control as conditions evolve.

To discuss how this situation could impact your supply chain, or to review practical routing and cost options, EMAIL Andrew Smith, Managing Director at Metro, for a direct and informed response.