Diplomatic efforts to reopen the Strait of Hormuz remain stalled, constraining one of the world’s most important energy corridors and prolonging the biggest disruption to global oil supply in decades.

Public statements from Tehran suggest Hormuz will only fully reopen once the conflict with the US and Israel is resolved, and even then Iran intends to retain a significant degree of control over traffic through the waterway.

Washington, for its part, is using an oil‑export blockade and secondary sanctions to squeeze Iran’s revenues and push it towards a ceasefire and broader deal. That has created a stand‑off, with Iran using threats to shipping and de facto control of Hormuz as leverage, while the US is using control of Iran’s oil exports and financial channels as its own bargaining chip.

Pakistan has tried to mediate between Washington and Tehran, hosting talks and shuttling ideas between the two sides, but recent rounds have produced little progress. Iran wants an end to the blockade and a clear framework for Hormuz governance before tackling nuclear issues, while the US wants concrete nuclear concessions up front, with maritime and sanctions relief later. That gap, combined with sporadic flare‑ups around the Gulf, is why many analysts now see a prolonged stand‑off or even a return to open conflict as real possibilities.

Oil and fuel markets stay tight

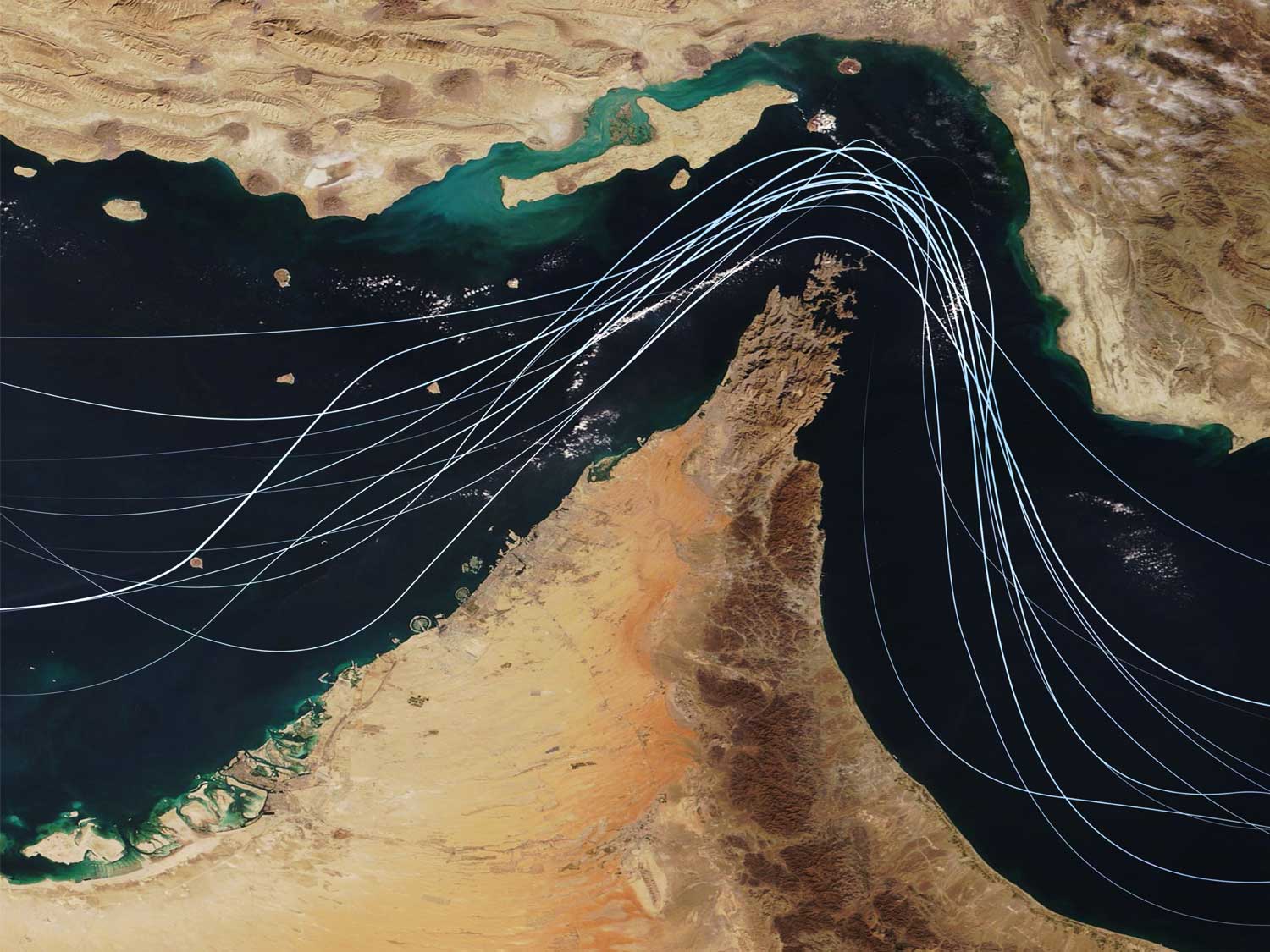

This deadlock is feeding directly into energy markets. Roughly a fifth to a quarter of global seaborne oil normally move through Hormuz, so any sustained disruption has an outsized effect on supply and sentiment. Since the start of the war, benchmark crude prices have jumped by around 50%.

Even partial diversions and intermittent tanker flows are enough to keep physical crude markets tight and refinery margins elevated. Refineries in Europe, the US and West Africa have shifted more output into aviation and marine fuels, but feedstock uncertainty and higher risk premiums are feeding through into bunker and jet prices. For carriers, that means bunker adjustment factors, emergency fuel surcharges and war‑risk charges are now key drivers of end‑user freight rates across ocean and air.

How this feeds into peak season

Higher oil and fuel prices ripple into every mode, and the timing of bunker adjustments now interacts directly with the traditional peak‑season calendar.

Historically, Asia–Europe peak season demand has built from late June through to China’s Golden Week in early October. In the last two years, that pattern was already starting earlier as shippers brought orders forward to deal with Red Sea diversions and longer voyage times. In 2024, Asia–Europe rates began climbing in early May and peaked by mid‑July; in 2025 the climb started in early June, again topping out around mid‑July.

This year, Hormuz‑linked fuel volatility adds another layer. Bunker costs spiked after the latest escalation at the end of February, prompting emergency surcharges on spot cargo and triggering higher quarterly bunker adjustment factors for contracts from 1 July. Many large shippers are now accelerating Asia–Europe shipments through May and June to move as much volume as possible before that quarterly BAF reset takes effect.

The result is a front‑loaded peak, with exceptionally strong demand in late May and June, driven by restocking needs and attempts to get ahead of fuel‑linked rate hikes. That demand sits on top of the disruption “premium” already visible in spot rates on key east–west trades, where prices are running several hundred dollars per 40ft above where seasonal patterns would normally put them.

For UK shippers, the geopolitical headlines around Hormuz translate into three practical realities:

- Fuel remains a structural driver of freight costs. Even if crude prices ease from day‑to‑day, bunker and jet markets are likely to stay tight and volatile as long as Hormuz is contested.

- Timing matters more than usual. Quarterly bunker adjustment dates and carriers’ general rate increase cycles are now key milestones; moving cargo just before a BAF reset can materially change landed cost.

- Peak season is starting earlier and lasting longer. Instead of a neat late‑Q3 surge, shippers face a longer high‑risk period running from late spring into the autumn, with rate spikes tied as much to fuel and conflict as to consumer demand.

Against that backdrop, we recommend that shippers should plan around higher and more volatile transport costs, rather than hoping for a quick return to pre‑crisis norms. Building in more lead time, watching bunker‑linked surcharges closely, and spreading volume across services and carriers can all help reduce the risk of being caught out by the next twist in Hormuz diplomacy.

EMAIL Managing Director, Andrew Smith, today to secure capacity, protect transit times and keep your supply chain moving in a rapidly changing environment.