With the container shipping lines diverting around Africa until the Red Sea maritime security situation improves, the uncertainty and unpredictability that surrounds schedules could fuel demand for air cargo as shippers seek stability of services and certainty of transit times.

Air cargo demand data for last month showed a 9% year on year increase, with spot rates reaching their highest level in nine months and the dynamic load factor increasing by 3% to reach 59%.

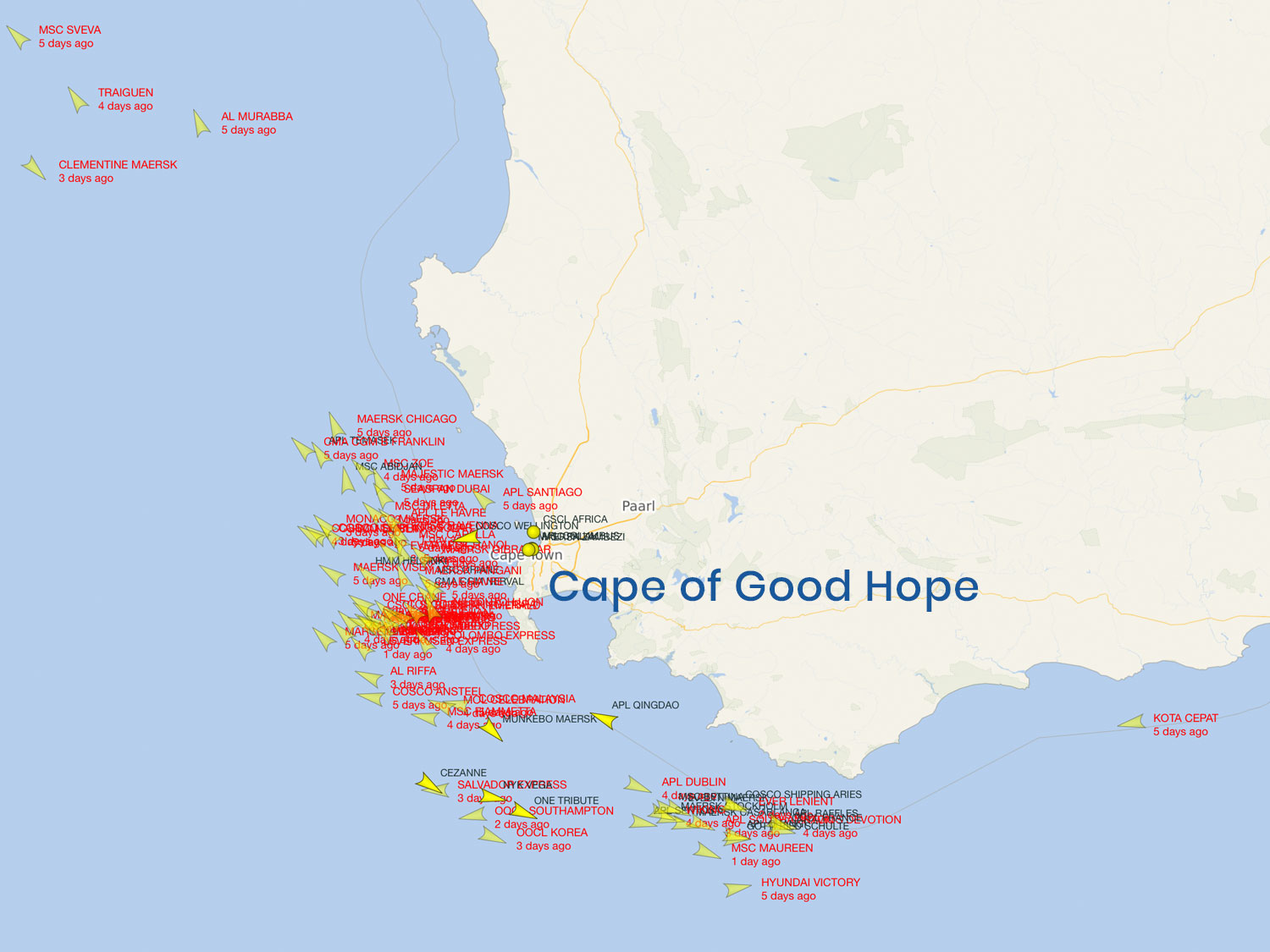

The Red Sea ship diversions around the Cape of good Hope will inevitably cause ships to cluster at ports, leading to port congestion, worsening equipment shortages and gaps in sailing schedules, which may significantly impact global supply chains.

Carriers will need to adjust schedules and networks, and would need to add more ships to achieve weekly or nearly weekly service frequency.

The diversion of ships away from the Suez Canal will swiftly see a million-plus containers delayed and when you factor in the knock-on effects of cash (in stock) tied up for longer, together with the fact that you don’t know how long this situation will continue means that some shippers will opt for the predictability of air cargo costing and reliability, to overcome the impact of the current sea freight disruption.

Improved stability in air cargo is encouraging a switch back to long-term, fixed-rate contracts, with deals for over six months rising to 45% of all contracts signed In the last quarter of 2023. Six-month contracts amounted to another 28% of the total market, while the share of up-to-one-month rates was just 14%.

This latest data appears to reflect stronger local market performance on key lanes and a global economy that is doing much better, but the market outlook forecast for 2024 remains modest, with an anticipated 1-2% growth in demand and a 2-4% rise in supply, though this does not take into account the potential ‘Red Sea’ effect.

Air cargo spot rates from Europe to the US were up +21% month over month in December, with the reduction in capacity helping to push up rates on this lane, while spot rates from China and Southeast Asia to Europe both rose 9% and strong eCommerce demand pushed the China to US air spot rate up 6% in December. Though these gains have subsequently fallen back, they may well recover if ocean shippers do start to look for time dependable alternatives, to hit supply chain deadlines.

Sea/Air; the effective and cost-efficient alternative

Sea/Air solutions offer an attractive blend of fast movement, defined transit times and significant economies over direct air freight.

The multimodal solution’s relative low-cost comes courtesy of a significant part of the cargo transit being undertaken by ship, from Asia, or the Indian subcontinent to Dubai, where cargo is transhipped securely and swiftly for the second transit leg, which is undertaken via air, directly to our UK hub airports, thereby completely avoiding the Red Sea problems and reducing transit times significantly.

Multimodal transport solutions like our Sea/Air solution are the best way for shippers to avoid delays between Asia and Europe and any potential land-side disruption.

Many of our customers are increasing the use of this solution, alongside their pure sea and air options, to avoid potential issues. We believe that Sea/Air should be considered to be a natural part of supply chain planning, due to the increased resilience and flexibility it offers over other modes and its lower carbon footprint compared to regular air freight.

For valuable, special and time-sensitive shipments we have a range of air freight and Sea/Air solutions, with extremely competitive rates and service combinations, to meet every deadline and budget requirement.

EMAIL Elliot Carlile, Operations Director, for insights, prices and advice.