Low-sulphur fuel container ship bunker prices have increased by a third since Russia’s move on Ukraine, with bunker surcharges rising around 15% and expected to spike further with crude oil hitting new highs of more than double the price at the beginning of the year.

Expect the carriers to claw back as much cash as possible in the form of emergency bunker surcharges and increased use of slow-steaming to mitigate the financial impact.

We are seeing delays and detention of cargo by overseas customs authorities seeking Russian and prohibited cargo and French customs officers have already seized two vessels suspected of breaching sanctions.

<Until trade lanes are free of Russian containers, disruption is to be expected, as customs intercede, cargo is identified, offloaded and (ideally, to free up much needed equipment) unloaded.

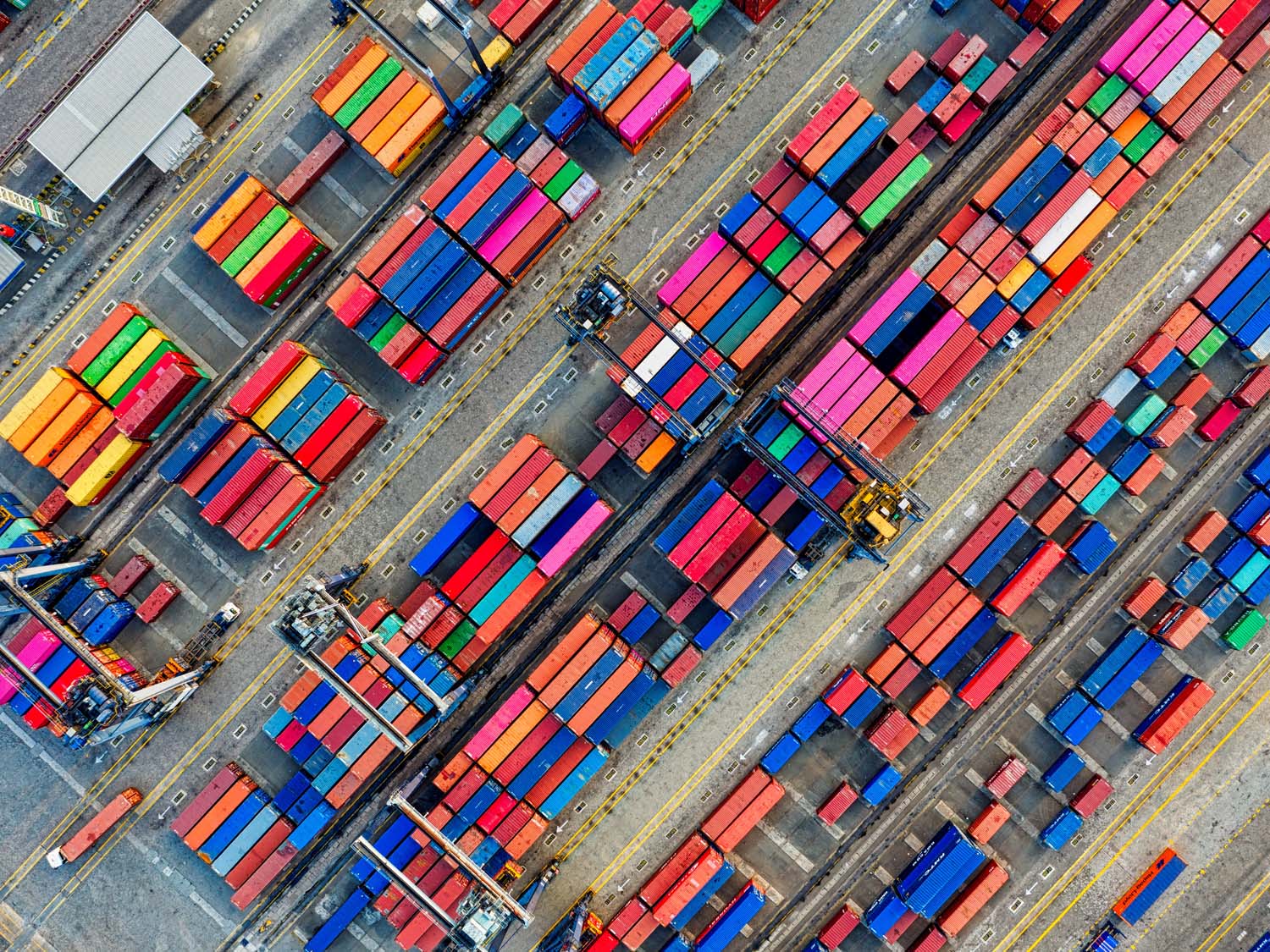

Dwell time for containers and vessels is a key indicator of port efficiency. The longer cargo is stuck in port, the more it potentially costs shippers, in rent, inventory holding and tied up working capital and container ships operate to stringent schedules, which means any delay ripples across the entire service.

During unexpected increases in dwell time, port operators increase stack heights and store containers on every available space in their yards, which significantly lowers productivity, potentially exacerbating dwell time.

Dwell times have increased 43% across Europe since Russia’s invasion of Ukraine, with consumer packaged goods, food and beverages, hit particularly hard, as dwell times increased by 55%.

Container ships are skipping ports to try and maintain their schedules or, at best, limit delays, which are averaging 17 days and unchanged since last November.

Average round trip duration for all seven OCEAN Alliance Asia - North Europe loops however stood at 93 days, compared to an average round voyage time of 78 days.

China to Europe rail freight operations are apparently continuing, though major service providers have added Moscow ally Belarus to their booking suspensions, which effectively blocks rail shipments on much of the Asia-North Europe network, because containers must be transferred to different gauge trains on entering Europe, with the busiest crossing at the Małaszewicze-Brest reloading area on the Poland-Belarus border.

Increasing in popularity with shippers, particularly for high-value products that would benefit from a faster transit, rail freight from China has grown massively since the advent of the COVID pandemic, with volumes surging 29% last year, to 1.46m teu.

The displacement of such massive volumes will have a profound impact on other modes from Asia, taking much needed capacity and putting even more pressure on pricing.

Air cargo shippers on Asia to Europe lanes, that are already anticipating a hike in prices as a substantial amount of capacity has come out of the market, as a direct result of Russia’s move on Ukraine, could be hit particularly hard.

Supply chains are facing a new set of challenges and with conditions changing rapidly, upstream and downstream, we are working closely with our network partners, to proactively identify potential issues and take any action necessary to protect our customers.

We maintain long-term contracts and space agreements with leading airlines, carriers and shipping lines, which means we can provide the best alternatives and options, whatever the situation.

Our proactive team, leading-edge technology and open communication, provide our customers with the real-time visibility, control and intelligence they need, to maintain resilient, flexible and reliable supply chains.